About Triple Bottom Line

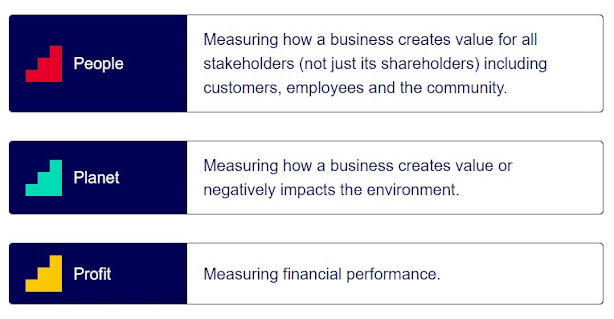

The Triple Bottom Line (TBL or 3BL) is known as a model created by John Elkington in 1994. It considers impacts of businesses in three dimensions: social, environmental and economic performance. The idea is often broken down into “people, planet, profit”. This helps to understand and track the economic, social and environmental value the organizations added or destroyed. Source: RMIT, Sustainability and Social Impact course, 2023 Sustainable development index is considered as the area where three dimensions overlap in the Sustainability Venn Diagram as shown below. The idea of achieving financial success and benefiting society drives the idea of creating shared value. The concept proposed by Michael Porter and Mark Kramer in a 2011 Harvard Business Review article says that businesses can look beyond corporate social responsibility (CSR) and improve profitability by considering social and environmental impacts in their strategies. This approach suggests that environmental or soc